Housing

Two stories from the data

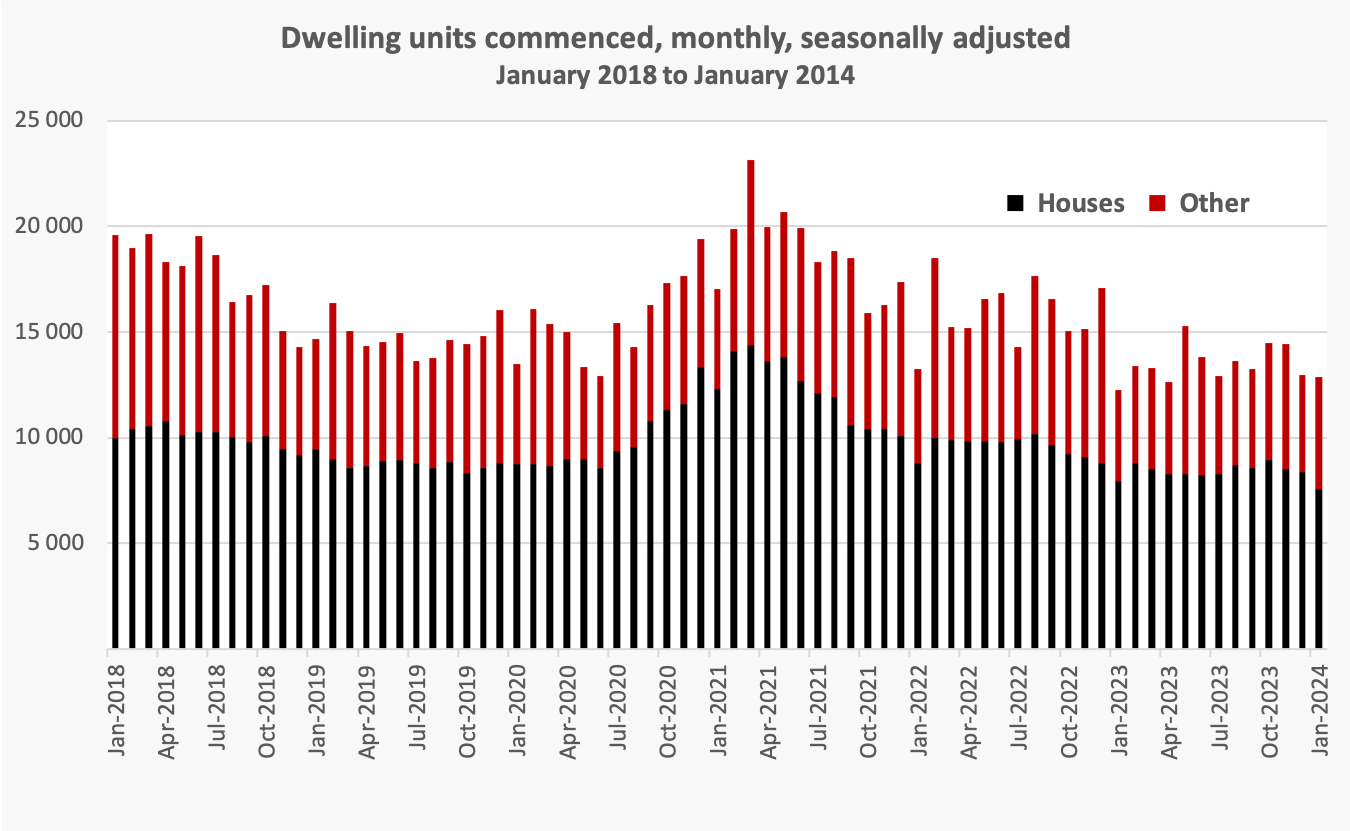

On Tuesday the ABS published its regular building approvals data, showing that from a peak of around 22 000 three years ago, the number of “dwelling units” (houses + apartments) approved has fallen to around 14 000 a month.

The fall in house commencements has been particularly steep, while approvals for “other” dwellings (mainly apartments) have held up a little better. The distinction is important because they are separate but overlapping markets, on both the supply and demand side. This difference in the markets is confirmed in the most recent CoreLogic Report Gap widens between house and unit values, showing that over the last twenty years house prices have risen much faster than apartment prices.

Approvals over the last six years are shown in the graph below.

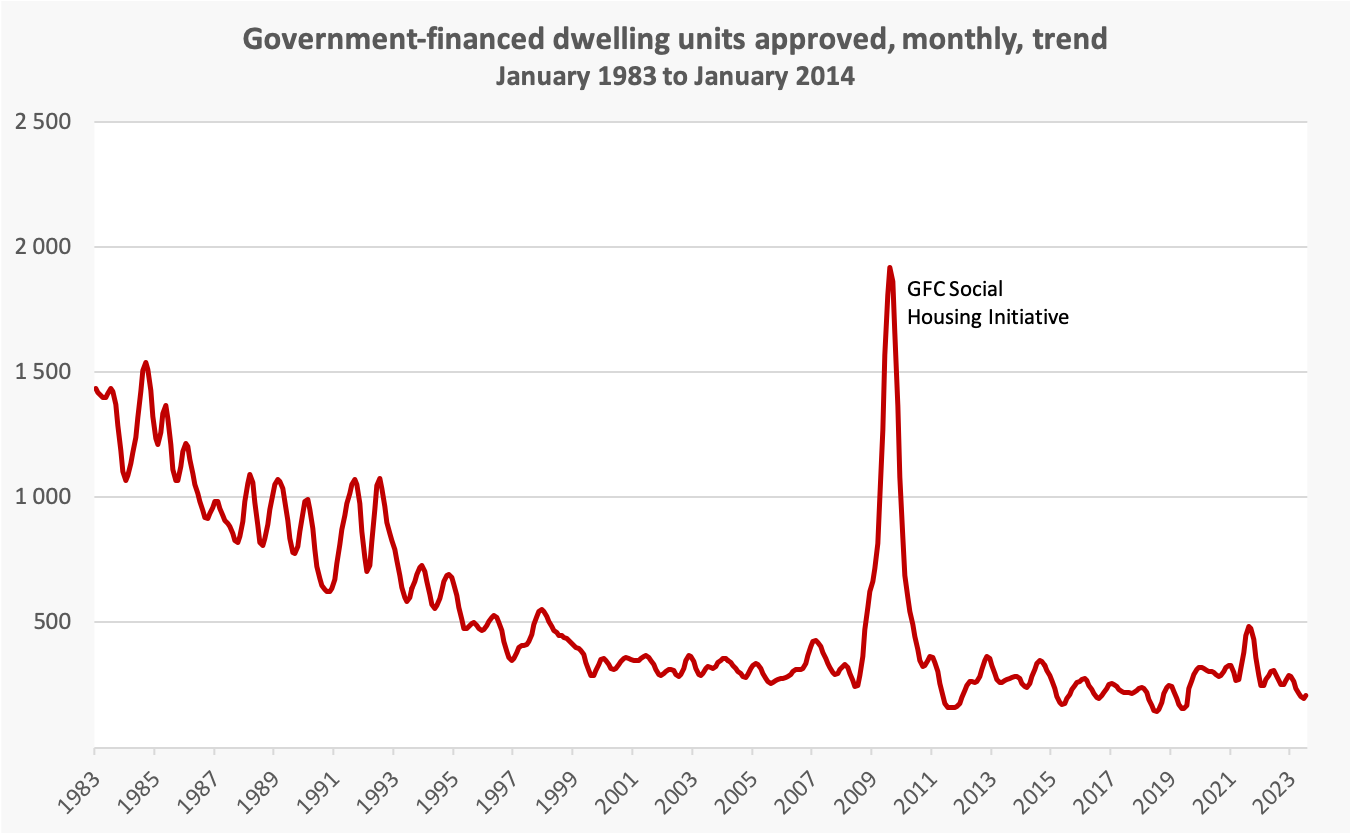

The other story on building approvals, in plain sight for many years but rarely covered by the media, is the long-term fall in approvals for public housing, shown below in a graph going back 40 years (the length of the ABS time series). The rate of approvals has fallen from about 1400 a month to about 300 a month, while the national population has almost doubled. It’s a long time since public housing made a large contribution to new housing approvals – in the 1980s its contribution was only about ten percent – but it has exercised a certain price restraint, particularly on the lower end of the market.

The Commonwealth’s Housing Australia Future Fund, recently passed after much bickering in the Senate, will boost public housing supply, possibly by around 500 a month according to Hal Pawson of the University of New South Wales. But it won’t restore public housing to its former prominence.

Anyone unfamiliar with Australia’s politics and accounting conventions would be puzzled by the Commonwealth’s reluctance to be more ambitious in providing public housing. For the government, housing is a solid investment. That’s because the Commonwealth can borrow at a lower interest rate than private builders, and in view of the fall in private approvals there would be resources available, meaning it shouldn’t be inflationary. If the Commonwealth were an ASX-listed company, the board would be announcing that it was confidently raising capital to make a sound investment.

The constraint is political, because over many years the fiscal cash outcome has been made into an indicator of the government’s economic management – an indicator that makes no economic or accounting sense, because it does not distinguish between capital and recurrent expenditure. Without that distinction, political attention to the cash deficit has constrained the Commonwealth’s capacity to borrow to strengthen the nation’s public asset base.

The situation is aggravated by accounting conventions. An outlay to the states to build public housing would be recorded as an expense on the Commonwealth’s books, even though in terms of a consolidated Commonwealth and state balance sheet, it would be an investment. That is why the Commonwealth has resorted to the limited earnings of the Housing Australia Future Fund as an accounting artefact to ensure it does not contribute to the cash deficit.

We won’t make progress on public housing until the Commonwealth Treasurer is able to announce that the Commonwealth is borrowing to make an economically responsible investment in making housing available for all Australians – as once was the core of the social wage. A pre-condition to granting the Treasurer that space is demolition of the idea that the Coalition is competent in economic management. That idea has been cultivated by the Coalition over many years, and reinforced by partisan journalists and gullible journalists with little understanding of economics or accounting,

The Greens’ housing policies – lofty ideas, but not well grounded

There has been an amount of media reporting on the Greens’ idea for the Commonwealth to become a property developer.

In concept it’s not radical. State governments took on that role in the “postwar era” 75 years ago. It’s supply-side oriented, which aligns with most economists’ assessment of present and medium-term priorities, and it would bring more competition to the market – a replication of the successful pattern of “benchmark competition” that saw entities such as the government-owned Commonwealth Bank exerting competitive pressure on the private banks.

Waiting for a policy

Beyond this general outline, however, all we have are a few scraps of detail, disclosed to the ABC’s Tom Crowley – Greens will call on federal government to develop property and sell it for cheap – and in a short ABC radio interview with the Greens’ spokesperson on housing, Max Chandler-Mather: Greens spruik plan for 600,000 government homes in a decade. From these we get the impression that there would be restrictions on eligibility for access to these homes, to buy or to rent, quotas on the number of houses to be sold and rented, and restrictions on re-sale. In these interviews there was a promise that the plan was to be launched at the National Press Club on Wednesday, but in that address all we heard in from Chandler-Mather was essentially an “ain’t it awful” presentation – as if anyone needed convincing. And there is no detail on the Greens’ website.

Nevertheless it is worth listening to the Press Club presentations, involving two 15-minute presentations, by Chandler-Mather and Mike Zorbas of the Property Council.

In the presentations there were predictable claims and counter-claims about property developers making excess profits and engaging in landbanking – withholding supply in order to sustain high prices.

Chandler-Mather framed capital-gains tax concessions and negative gearing as “subsidies” to property developers, designed as a deliberate bipartisan policy to keep house prices high to benefit property developers. There is no doubt that they have contributed to high prices, have distorted investors’ choices, and have been unfair, but the suggestion that the Albanese government is deliberately aiming to keep property prices high verges on paranoia. The more reasonable accusation against the government is about a lack of political courage. Also, the Greens need to put up realistic proposals on capital gains tax: abolishing or reducing the valuation discount (presently 50 percent) without restoring indexation, would retain the incentive for investors to continue to use real-estate for fast- turnover speculation.

In contrast to Chandler-Mather’s emotive style, interspersed with the occasional uncontextualized figure, Zorbas gave a disciplined presentation, focused on the need to boost supply (hardly the stance of a monopolist), and starting with the present problems in the industry. These problems include a high rate of household formation, entrenched low-productivity practices, zoning, climate change, rising prices of materials, and competition for workers with building and construction skills.

He went on to outline a nine-point plan to boost supply. Most elements are uncontentious (some would call his ideas left-wing), apart from issues to do with planning and zoning, and taxation.

On planning and zoning the issues are about NIMBY politics, and inflexibility and delays in the approvals process. On taxation the main issue seems to be about stamp duty. Both of these are in the hands of local and state governments. The equity considerations around these issues is a common one – the interest of established house-owners versus those who are seeking to become house-owners.

Zorbas suggested that if governments were to collect so much tax from housing, it would make sense to hypothecate that tax to helping boost supply, particularly for those most in need.